EU Securitisation Reform: What is changing and what comes next?

The European Parliament has published its draft report on proposed amendments to the EU securitisation framework (covering both CRR and SecReg), marking a key step towards restoring securitisation as an effective tool for risk transfer and capital management.

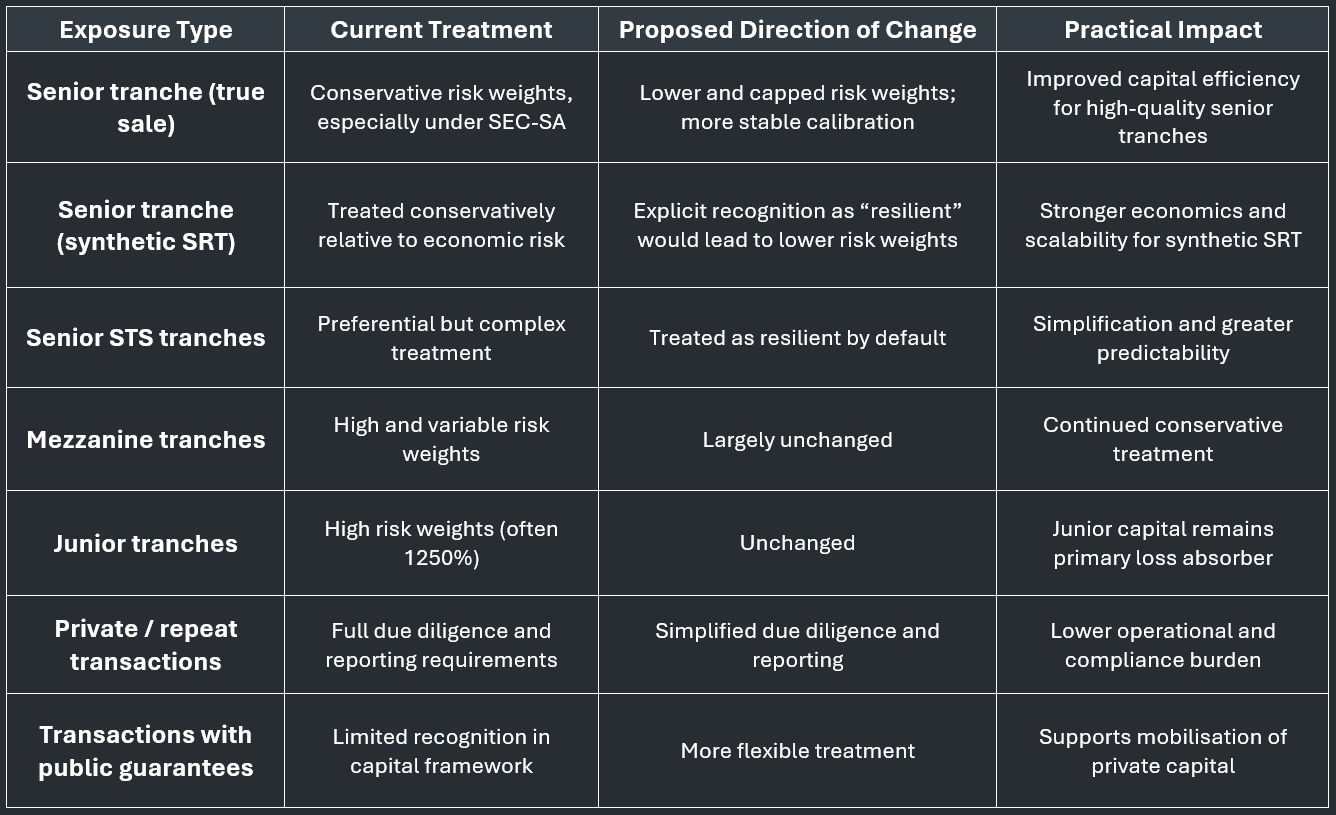

The draft report supports lower, more risk-sensitive capital charges, particularly for senior tranches, and introduces simplifications to the operational elements of securitization transactions (including streamlined due diligence for repeat issuances and reduced reporting requirements for granular portfolios, among other things). The intention is to lower operational barriers without weakening supervisory oversight. Senior tranches will also benefit from only having to be assessed at origination (rather than on an ongoing basis), significantly reducing capital volatility over the life of a transaction.

The Parliament also supports the European Commission’s proposal to introduce a new category of so-called “resilient” securitisations. The concept is recognised as being mostly relevant for synthetic securitisations, whereas for traditional securitisations it is acknowledged that the existing STS framework already provides an adequate quality indicator.

As a result, these proposals will:

· Preserve and simplify the resilience concept for synthetic securitisations, and

· Avoid introducing additional layers of complexity for traditional STS transactions.

In addition, securitisations backed by public or promotional guarantees will benefit from more flexible risk-retention and due-diligence treatment where first-loss protection is provided by EU or national institutions, supporting the flow of private capital into policy-relevant asset classes.

The table below provides an overview of the key anticipated changes to the securitisation regulatory landscape.

Table1: Comparison of Proposed Changes to Securitisation Risk Weights

To summarize:

The reform is directionally positive, particularly for synthetic securitisations. The draft report acknowledges the role of synthetic SRT as a balance-sheet and capital management tool, and more stable, proportionate capital treatment, combined with simplified compliance requirements, should improve predictability, economics and scalability of synthetic transactions.

Taken together, the changes are likely to:

· Enhance the attractiveness of synthetic SRT for senior investors,

· Improve capital efficiency for originating banks,

· Support a broader use of synthetic securitisation across asset classes, including mortgages, SMEs and specialised lending.

What happens next?

The European Commission’s proposal marked the starting point of the legislative process, with the Parliament’s draft report being the next formal step. Now follows:

While political agreement may be reached during 2025, the amended rules are most likely to be finalised and implemented during 2026, with customary transitional periods before coming into full effect.

For market participants, the reforms have the potential to materially improve the attractiveness of, in particular synthetic, securitisations, both from an economic and a regulatory perspective.